As we move through the first quarter of 2026, the construction landscape in the USA, UK, and Canada is being reshaped by a new era of “Construction Cost Estimating (C.C.E).” The days of pandemic-induced chaos have faded, replaced by complex geopolitical pressures and a shift toward high-tech infrastructure. For developers and contractors, the ability to pivot based on real-time data is no longer a luxury; it is a survival skill.

In the current market, the global construction material price index has become a central focus for every boardroom discussion. While some materials like lumber have found a precarious floor, others like steel are being propped up by significant trade barriers. Navigating these shifts requires a sophisticated approach to [suspicious link removed], where historical data must be balanced against today’s rapid-fire economic headlines and localized supply chain disruptions.

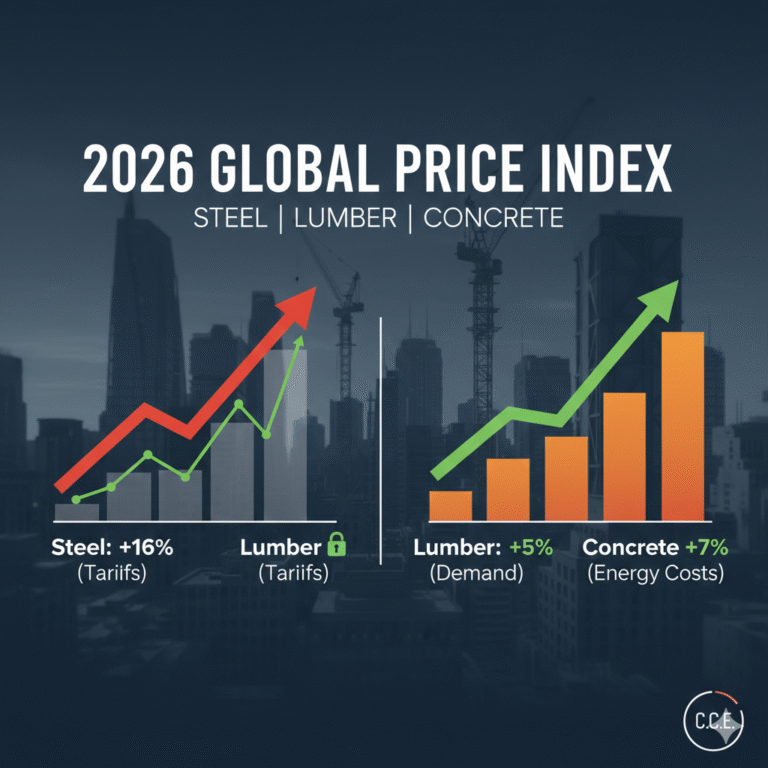

Steel: The Impact of 50% Tariffs and High-Tech Demand

Steel remains a highly volatile variable in the 2026 budget. In the United States, the implementation of a 50% tariff on imported steel and aluminum has sent ripples through the supply chain. While domestic mills are operating at steady capacity, they have raised prices to match the new tariff-adjusted baseline, forcing estimators to rethink their procurement strategies.

Beyond policy, the global explosion in AI data centers and semiconductor manufacturing facilities has created a massive backlog for structural steel fabricators. Many large-scale shops are already booked through late 2026, leading to extended lead times.

- USA: Hot-rolled coil (HRC) steel hit a 24-month high in February 2026, trading near $980/ton.

- UK: Steel rebar has seen a slight annual cooling of approximately 8%, providing a rare window of relief for masonry-heavy projects.

- Canada: Strong infrastructure spending in Ontario continues to keep structural beam pricing firm.

Lumber: A Seasonal Recalibration Amid Trade Disputes

Lumber has recently been the “stable” child of the commodity family, but that stability is being tested. As of February 2026, framing lumber is trading around $568/MBF (thousand board feet). This downward trend is largely due to a seasonal slowdown in residential housing starts across North America.

Yet, there is an undercurrent of tension. Ongoing duties on Canadian softwood lumber—currently sitting near 45% for some exporters—prevent prices from dropping back to pre-pandemic levels. Many mills across the Pacific Northwest operated at a loss for much of 2025, leading to curtailments that have tightened the supply as we approach the spring building season.

For those tracking the global index, lumber is currently a “buy now” opportunity. Once warmer weather hits and interest rate cuts begin to stimulate the housing market, a 5-10% price correction is expected by Q2.

Concrete and Cement: Steady Upward Pressure

Concrete is often overlooked in price discussions because it doesn’t experience the 200% swings seen in lumber. However, its steady climb is what often breaks a budget. In 2026, ready-mix concrete pricing has risen by 6-8% year-over-year in most major urban centers.

The primary drivers here are energy and logistics. Cement production is carbon-intensive; as producers invest in “green cement” technology to meet 2030 climate goals, those capital costs are being passed down the line. Furthermore, specialized labor shortages in the ready-mix sector have forced firms to increase wages, adding an invisible layer of cost to every cubic yard poured.

Global Concrete Market Snapshot (2026)

| Region | Price Movement (YoY) | Primary Market Driver |

| USA | +7.2% | Infrastructure Bill & Data Center Expansion |

| UK | +4.5% | Energy Surcharges & Carbon Taxes |

| Canada | +6.1% | Urban Density Projects & Logistics Costs |

Strategic Bidding in a Volatile 2026

The complexity of the current market has fundamentally changed how we approach the tender process. Relying on static spreadsheets is a recipe for disaster. Professional estimators are now incorporating “escalation clauses” into contracts, allowing for price adjustments if key materials swing more than 5% during the project lifecycle.

Expertise in this area is more critical than ever, and resources like The Definitive Guide to Construction Cost Estimating in 2026 provide the necessary framework for building these contingencies into your bids. The goal is to move from reactive “firefighting” to a proactive strategy where risk is shared and your profit is protected.

Frequently Asked Questions

Why are steel prices rising despite a seasonal slowdown?

Steel prices are currently driven more by trade policy (tariffs) and massive infrastructure demand from data centers than by traditional residential cycles. This creates a high price floor that persists even during slower months.

How do interest rate cuts affect the material price index?

Lower interest rates typically lead to an increase in housing starts. This surge in demand puts immediate pressure on lumber and drywall prices, often leading to a spike in the second and third quarters of the year.

What is the current lead time for structural steel in 2026?

For many large fabricators in North America, lead times are currently 6 to 10 months. Securing material early is essential for project timelines.

Is “Green Concrete” significantly more expensive?

In the current 2026 market, low-carbon concrete mixes can carry a 5-12% premium. However, many government-funded projects in the UK and Canada now require these materials, making them a standard line item in many bids.

How can I protect my bid from price spikes?

Effective methods include using formal indexed pricing tied to benchmarks, including escalation clauses in your contracts, and diversifying your supplier list to avoid regional bottlenecks.